Jul 28, 2025

Follow us on Google for more Money.ca news

Add us on GoogleEven as inflation continues to squeeze household budgets and on the eve of another Bank of Canada rate announcement, Canadians are pointing fingers over who should act to tackle the country’s growing debt crisis.

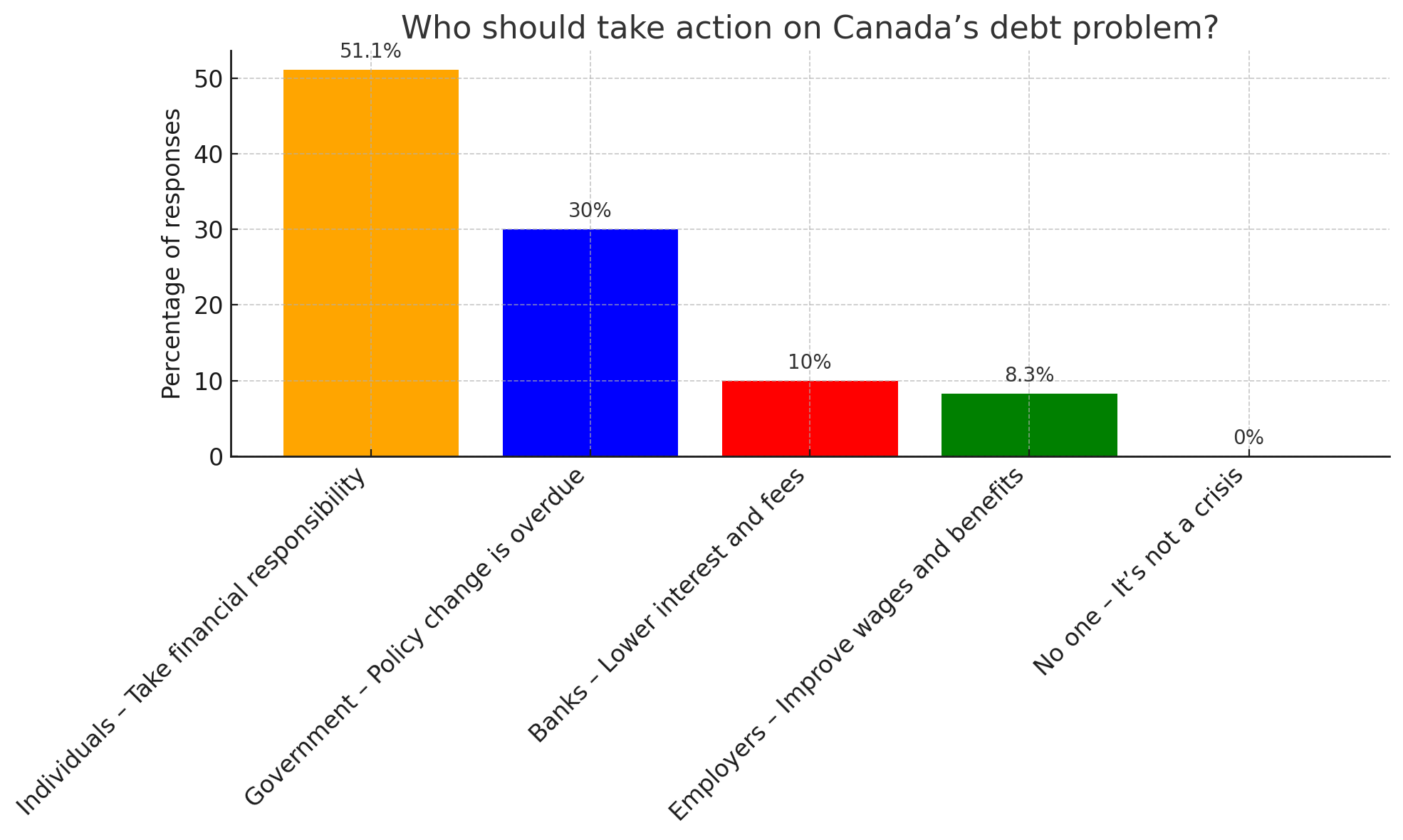

According to a Money.ca reader poll, more than half of respondents (51.1%) believe it’s up to individuals to take financial responsibility. Survey results reveal that while Canadians acknowledge institutional responsibility, most believe the solution starts at home.

Financial burden shifting to individuals

The data comes amid continued financial stress for Canadians, with grocery prices still elevated, mortgage renewals looming at higher rates, and national household debt nearing $2.9 trillion according to Statistics Canada. With limited relief in sight, many Canadians are being forced to confront their personal spending, budgeting, and borrowing habits.

Thanks for subscribing!

The best of Money.ca delivered weekly.

By signing up, you accept Money.ca Terms of Use, Subscription Agreement, and Privacy Policy.

These survey results may show that despite the desire to take responsibility for spending — and saving — this is hard for Canadians when wage growth hasn't kept up with inflation. Still, the sentiment that cost-cutting starts at home may show that many Canadians believe that others are living beyond their means — and that credit card bills are catching up.

Must Read

- Warren Buffett used these 4 solid, repeatable money rules to turn $9,800 into a $150B fortune. Here’s how to apply them to your own life

- Stop the leak: 5 costs Canadians (still) overpay for every single month. How many are sabotaging your 2026 budget?

- Three in four Canadians say their insurance premiums have increased in the last two years. Compare 20+ quotes on Rates.ca and save up to 20% when you bundle home and auto

Join 19,000+ readers and get Money.ca’s best stories and exclusive interviews first — clear insights curated and delivered weekly. Subscribe now.

Government and banks still in the hot seat

While 51.1% of respondents placed the onus on individuals, nearly one-third (30%) said the federal government needs to step in with policy changes — such as implementing stricter borrowing regulations or increasing housing affordability measures.

Advertisement

Another 10% blamed banks, calling on them to lower interest rates and reduce consumer fees.

A smaller group (8.3%) pointed to employers, saying better wages and benefits would help Canadians keep up with the cost of living.

Only a negligible number indicated that no one needs to take action, suggesting most Canadians see the debt load as a serious issue.

A pivotal moment for the Bank of Canada

This conversation around debt comes at a time of high public interest in the Bank of Canada’s next move. While the central bank held its overnight rate in June 2025 — and many economists predict another rate hold in July 2025 — the probability of a rate cut in the fall is trending higher.

While rising living costs continue to squeeze Canadians, most analysts predict a rate hold for July because of the emphasis Bank of Canada Governor Tiff Macklem puts on “persistent cost pressures” — including housing and insurance premiums and the impact of global conditions, including tariffs. As a result, these uncertain pressures could delay a BoC rate reduction, for the moment.

A wake-up call

Unfortunately, the cautionary tone reinforces the feeling among Canadians that they’re largely on their own when it comes to getting their financial houses in order.

As such, survey results may signal a growing frustration regarding a lack of coordinated action from institutions, including the Bank of Canada; it may also highlight a shift in public sentiment with many Canadians no longer convinced that a government fix is coming prompting to a more inward solution, instead.

This inward shift means that financial literacy, among all Canadians, may be the difference between stability and stress — as right now there is little confidence in a coming safety net.

Survey methodology

The Money.ca newsletter survey was conducted through email in May 2025. Approximately 6,310 email newsletter subscribers, over the age of 18, were surveyed resulting in 180 responses. The estimated margin of error is +/- 6%, 19 times out of 20.

About Money.ca

Money.ca is a leading financial platform committed to providing individuals with comprehensive financial education and resources. As part of Wise Publishing, Money.ca is a trusted source of reliable financial news, expert advice, comparison tools and practical tips. Canadians get insight on a variety of personal financial topics, including investing, retirement planning, real estate, insurance, debt management and business finance.

Sources

1. Statistics Canada The Daily

You May Also Like

- This 7-step plan from Dave Ramsey is designed to help you ditch debt, save more and build wealth — here’s how it works

- Prioritize these 4 critical investments and watch your net worth skyrocket

- Focus on these 3 ‘magic numbers’ to become a millionaire — and only on these numbers. How do you stack up?

- Millionaires under 43 are reshaping investing — just 25% of their portfolios are in stocks. Here’s where their money is going

The most expensive financial mistakes are often the ones you don't see coming. Join 19,000+ Canadians who get the money moves, risks and opportunities shaping their finances — delivered free each week. Subscribe now.

Romana King, Senior Editor at Money.ca, also writes for various North American publications and the RKHomeowner blog. Her book, House Poor No More, is an Amazon bestseller and five-time award winner, including the 2022 New York CPA Society's Excellence in Financial Journalism (EFJ) Book Award.