Mar 26, 2025

Follow us on Google for more Money.ca news

Add us on GoogleIn today’s globalized world, savvy travellers know that smart currency management can make or break a trip. As we navigate the travel landscape of 2025, understanding the ins and outs of currency exchange is more crucial than ever. Whether you’re planning a shopping spree in Tokyo, a culinary tour in Mexico City, or a cultural expedition in Seoul, this guide will help you maximize your Canadian dollars and avoid common pitfalls.

The current currency landscape

Before we dive into the nitty-gritty of currency exchange, let’s take a quick look at the current state of affairs:

Thanks for subscribing!

The best of Money.ca delivered weekly.

By signing up, you accept Money.ca Terms of Use, Subscription Agreement, and Privacy Policy.

- The Canadian dollar remains strong against many currencies, particularly in popular destinations like Japan, Mexico, and South Korea.

- International travel is on the rise, with 77% of travelers planning to venture abroad in 2025.

- Millennials and Gen Z travelers are leading the charge, focusing on meaningful, culturally rich experiences.

Top methods for exchanging currency

1. Use credit cards wisely

Credit cards remain the gold standard for international purchases, offering convenience and often the best exchange rates. However, not all cards are created equal.

Pro Tip: Opt for a no foreign transaction fee credit card. Our top picks include:

These cards can save you the typical 2.5% to 3% foreign transaction fee, putting more money back in your pocket for souvenirs or that extra special meal.

Read More: Best no foreign transaction fee cards

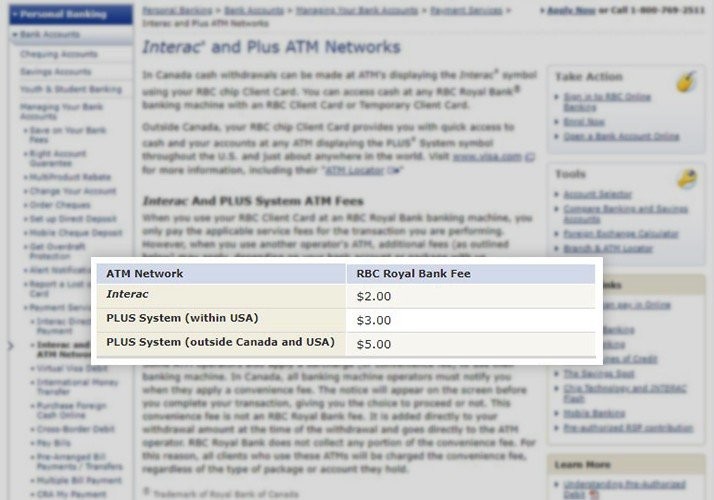

2. ATM withdrawals: A necessary evil

While credit cards should be your go-to, having some local cash is often unavoidable. ATMs generally offer better rates than currency exchange offices, but be mindful of fees.

RBC’s ATM fees. Note the higher charge for international withdrawals

Money-Saving Strategy:

- Use bank-affiliated ATMs to minimize fees

- Make fewer, larger withdrawals to reduce transaction costs

- Check if your bank has international partners for reduced or waived ATM fees

3. Currency exchange services: Choose wisely

If you must use a currency exchange service, do your homework:

- Compare rates with the Bank of Canada’s currency converter

- Check rates at your bank (but don’t assume they’re the best)

- Research local currency exchange offices at your destination

- Avoid airport kiosks and tourist area exchanges like the plague

Expert Insight: We’ve found that well-researched currency exchange offices can offer rates up to 1.5% to 5% better than banks.

Avoiding common currency exchange pitfalls

Beware of ‘Dynamic currency conversion’

This sneaky practice allows merchants to charge you in Canadian dollars instead of the local currency. It might seem convenient, but it often comes with a hidden markup.

Rule of Thumb: Always choose to pay in the local currency when given the option.

Don’t over-exchange

With the rise of digital payments and the increasing acceptance of credit cards worldwide, you might need less cash than you think.

Smart Traveler Tip: Start with a small amount of local currency and top up as needed. This approach minimizes the risk of being stuck with excess foreign cash at the end of your trip.

Leveraging technology for better currency conversion rates

In 2025, fintech solutions are making currency exchange easier and more cost-effective:

- Mobile Banking Apps: Many now offer real-time exchange rates and the ability to lock in rates before you travel.

- Digital Wallets: Services like Apple Pay and Google Pay are increasingly accepted internationally, often with favorable exchange rates.

- Currency Exchange Apps: These can help you find the best rates in real-time at your destination.

The bottom line

As we navigate the travel landscape of 2025, smart currency management is key to stretching your travel budget. By leveraging no foreign transaction fee credit cards, being strategic with ATM withdrawals, and staying informed about exchange rates, you can focus on what really matters – creating unforgettable travel experiences.

Remember, the best currency exchange strategy is the one that combines convenience with cost-effectiveness for your specific travel needs. Happy travels, and may your Canadian dollars take you further than ever before!

Read more: Canada's best credit cards

Conditions Apply. Visit the card provider’s website for complete card details, terms, and current offers. Reasonable efforts are made to maintain accuracy of information, but all credit card details are subject to change.

Cory Santos is a finance writer, editor and credit card expert with nearly a decade of experience in personal finance. Cory joined Wise Publishing from BestCards, with bylines in numerous print and digital publications across North America, including the Miami Herald, BlogTO, Debt.ca, AOL, MSN and Medium as well as financial podcasts like KOFE Talk. He's also the creator and author of the annual Money.ca Credit Card Awards.

Credit Cards • Jul 02

Best card combinations for earning cash back and rewards

Credit Cards • Dec 10